- 13 mins

What if the four walls protecting your family are more vulnerable than you think? You’ve spent years building your life’s work within your home, yet rising property taxes in 2026 often feel like a constant drain on your legacy. It’s natural to feel frustrated by the complex homestead exemption rules or worried that a legal setback could threaten your family’s sanctuary.

We agree that your home should be your most secure asset, not a source of anxiety or confusion. This guide explains how to use these tax laws to lower your annual bill and create a legal shield for your primary residence. You’ll learn how this simple filing can save homeowners an average of $1,200 per year while keeping your property safe from creditors or lawsuits. We will cover exactly how to qualify, how to avoid common filing mistakes, and the practical steps to lock in your protection for the next generation.

Key Takeaways

- Understand how a homestead exemption lowers your property tax bill by reducing your home's taxable value.

- Learn how to transform your family home into an unshakeable fortress that creditors and debt collectors cannot easily take away.

- Discover the specific residency and ownership requirements you must meet to secure these vital legal protections.

- Identify the essential records you need to store in a digital vault to ensure your heirs can always prove the home's protected status.

- Avoid common application mistakes that could leave your family’s most important asset vulnerable to unnecessary taxes.

What Is a Homestead Exemption?

Imagine waking up to find that a sudden financial crisis threatens the roof over your children's heads. A homestead exemption acts as a legal fortress around your primary residence. It ensures that even in the face of economic hardship, your family has a place to call home. This provision protects a portion of your home's value from property taxes and certain creditors. It's more than just a tax break; it's a commitment to your family's long-term stability.

To qualify for this protection, the property must be your primary residence. This means you live there for the majority of the year and consider it your permanent base. Vacation homes or investment properties don't qualify for these benefits. In states like Florida, you must reside in the home on January 1st of the tax year to claim the benefit for that cycle. Proving occupancy is the first step in securing your legacy.

These laws have deep roots in American history. The first homestead law was passed in Texas in 1839. Lawmakers created it to prevent families from losing everything during the economic instability that followed the Panic of 1837. They realized that keeping families in their homes was better for the community than allowing creditors to seize every asset. Today, this protection is a foundational part of a modern estate plan. It’s the first layer of defense for your family's heritage and financial health.

The Two Main Types of Homestead Protection

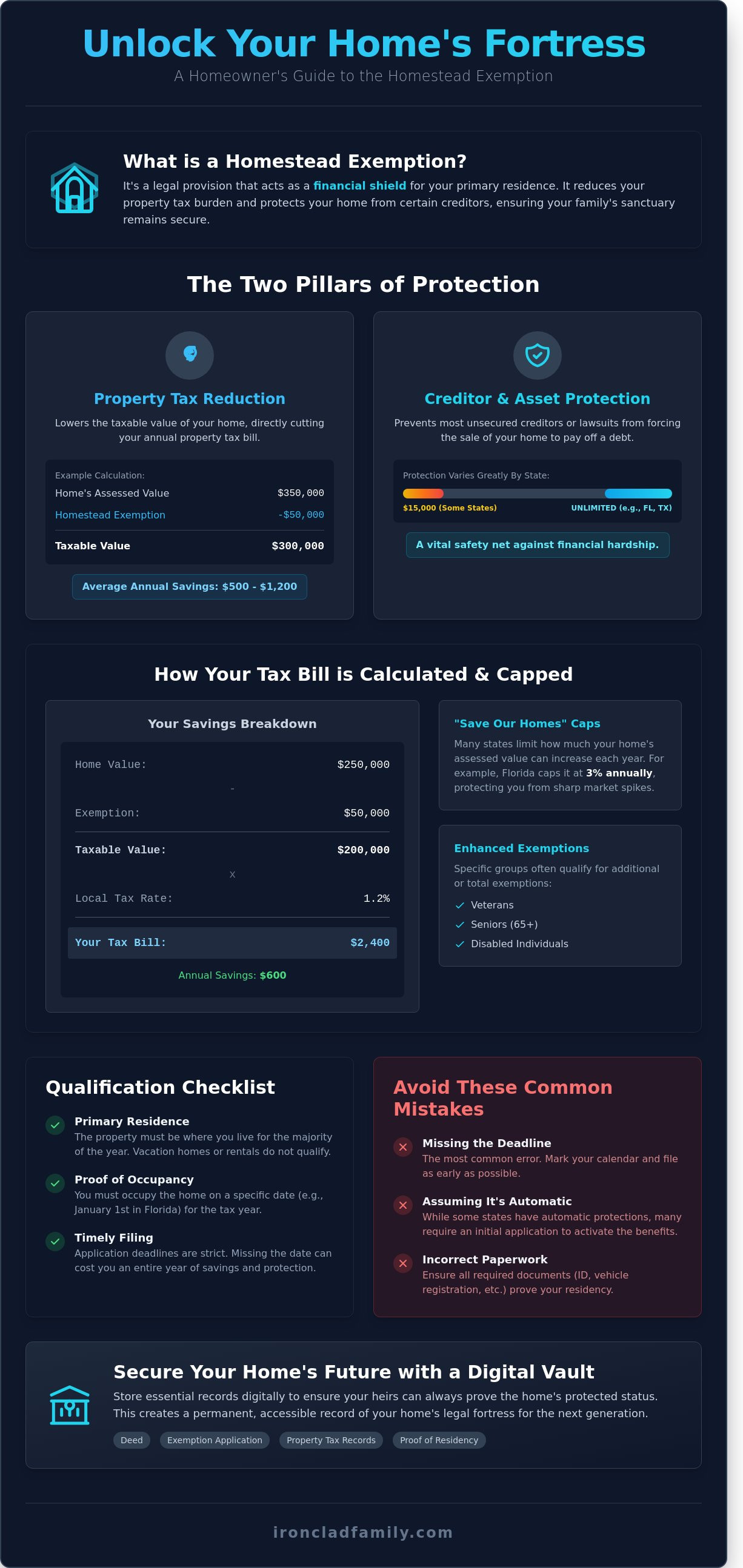

Property tax exemptions lower the taxable value of your home. If your house is valued at $350,000 and you have a $50,000 exemption, you only pay taxes on $300,000. This often saves homeowners between $500 and $1,200 every year. Asset protection works differently. It prevents a creditor from forcing the sale of your home to pay off a debt. Some states, like California, provide automatic protections, while others require a formal filing with the county recorder to activate your shield.

Key Takeaways for Homeowners

- Occupancy is mandatory: You must live in the home as your main residence to be eligible for any level of protection.

- Tax savings are significant: The exemption can lower your annual property tax bill by a fixed dollar amount or a percentage of the home's value.

- Creditor defense: It provides a vital safety net against most unsecured creditors and civil lawsuits.

- Deadlines matter: Missing a state filing deadline by even one day can cost you a full year of savings and protection.

- State rules vary: Protection levels range from $15,000 in some states to unlimited equity protection in others like Florida or Texas.

Understanding the homestead exemption is about more than just numbers on a tax return. It's about creating a secure environment where your family can thrive without the fear of losing their foundation. By taking the time to file the correct paperwork, you're placing a protective vault around your most valuable physical asset.

How the Homestead Exemption Reduces Your Tax Burden

Protecting your family's financial legacy starts with understanding your home's true cost. The homestead exemption acts as a legal shield for your primary residence. It works by creating a gap between what your home is worth and what you actually pay taxes on. To understand this, you need to know the difference between assessed value and taxable value. The assessed value is the dollar amount a county appraiser places on your property. The taxable value is the final number used to calculate your bill after all exemptions are subtracted.

Most states provide this relief in two ways. Some use a fixed dollar amount, such as knocking $25,000 or $50,000 off your assessment. Others use a percentage-based reduction. Beyond these initial cuts, many regions employ "Save Our Homes" style caps. These laws are powerful tools for long-term security. They limit how much your home’s assessed value can increase each year, regardless of how fast the local real estate market grows. In Florida, for example, this cap is often limited to 3% annually. This prevents families from being priced out of their own neighborhoods by rising property values.

Specific groups receive even stronger layers of protection. Veterans with service-connected disabilities, seniors over age 65, and individuals with permanent disabilities often qualify for additional credits. These specialized exemptions can sometimes wipe out a property tax bill entirely. It's a way for the community to honor service and protect those on fixed incomes.

Calculating Your Potential Savings

Let’s look at a concrete example. If you own a $250,000 home and qualify for a $50,000 exemption, your taxable value drops to $200,000. If your local tax rate is 1.2%, you save $600 every year. You should pay close attention to how school district taxes are handled. In many jurisdictions, school taxes only recognize a portion of the homestead exemption, meaning your savings might vary across different parts of your tax bill. Review your statement every year to confirm these credits are still being applied correctly.

The Impact of Inflation on Property Taxes

Inflation is a persistent threat to family stability. By the year 2026, several states expect to adjust their exemption thresholds to account for the rising cost of living. Staying informed about these local law changes is a core duty of a Digital Guardian. You aren't just managing paper; you're defending your family's future. It's wise to store your historical tax assessments and exemption approvals in a secure digital vault for families. This ensures you have a permanent record to challenge unfair hikes or prove your eligibility if the county records are ever lost. Keeping these records organized allows you to move from a place of uncertainty to absolute preparedness.

Qualifying and Applying: Requirements and Common Mistakes

Securing your home's future starts with meeting basic rules. You must hold the legal title to your property. In most states, like Florida or Texas, you need to own the home by January 1st of the tax year. If you close on your house on January 2nd, you usually have to wait another full year to save. Timing is everything here. This hard rule costs families thousands of dollars every year.

Proving you actually live there is the next step. Tax assessors look for your permanent intent to stay. They will check your driver's license address and your voter registration. If these don't match your home address, your application will likely be denied. Utility bills from the last 90 days also serve as vital evidence of your residency. Don't leave these details to chance.

Missing a deadline is the most common reason people lose their homestead exemption. In many jurisdictions, the filing window closes on March 1st or April 1st. If you miss this date by even one day, the county won't give you the discount. You can't just apply once and forget it if you move. You must reapply for every new primary home you buy.

Avoid common traps like double dipping. You can't claim an exemption on a vacation home in another state. If you rent out your primary home for more than 30 days in some areas, you might lose your status. This protection is for your family's roof. It's not for a business venture. Check your deed now to ensure your name is listed correctly.

Documentation You Will Need to Apply

Gathering your records early prevents stress. You'll need your recorded deed or trust documents to prove ownership. Every owner listed on the title must provide their Social Security number. Most offices also ask for your previous year’s tax returns or recent utility statements to confirm you live on the property full-time. Keep these in a safe place. Having them ready ensures a smooth application process.

Homestead Exemptions and Living Trusts

Moving your home into a trust is a smart way to protect your legacy. It ensures your house stays in the family. However, it can complicate your tax status. You must ensure the trust document includes specific language. It needs to show you keep equitable title or the right to live there for life. Without these words, the tax office might see the trust as a separate owner and deny your homestead exemption. When planning your estate, you should understand the difference by Choosing between a trust and will to keep your benefits safe.

Homestead Exemptions as an Asset Protection Tool

A homestead exemption does more than lower your annual property tax bill. It acts as a primary defense for your family's most important physical asset. If you face a lawsuit from a credit card company or a medical provider, these laws can prevent a forced sale of your home. Think of it as an unshakeable fortress. While other assets might be vulnerable, your house remains the last thing creditors can reach. This protection ensures your family's physical heritage stays secure even during financial storms.

Security has its limits. A homestead exemption won't stop a mortgage lender from foreclosing if you miss payments. It also doesn't provide a shield against the IRS for unpaid federal taxes. Knowing these boundaries is vital for true peace of mind. You aren't just protecting a building; you are safeguarding the place where your family's story unfolds. This emotional security is just as valuable as the financial benefits.

State-by-State Variations in Protection

Every state handles these protections differently. Florida and Texas offer 100% unlimited value protection, meaning the entire equity of your home is safe regardless of its price. In contrast, states like California use a sliding scale between $300,000 and $600,000 based on local median home prices as of 2021. You need to know your specific state's exempt amount to plan effectively. This data should be a core part of your family preparedness service records to ensure your legacy remains intact.

When Homestead Protection Fails

Protection isn't absolute. If you move large sums of money into your home just to hide it from a pending lawsuit, a court might call this "fraudulent conversion." In these cases, the shield may vanish. Bankruptcy also complicates things. Under the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005, you must live in a state for at least 1,215 days to claim its full homestead exemption. For complex asset protection needs, it's wise to consult a professional who understands these legal nuances. Keeping your documents organized ensures you have the proof needed to defend your home when it matters most.

Protect your family legacy by setting up a secure digital vault for families today.

Securing Your Home’s Future with a Digital Vault

Your home is more than just a building. It's the foundation of your family's future and the center of your life's work. The homestead exemption is a vital part of what we call your "Digital DNA." This information tells the story of your home's legal and financial status. It's the proof that you've secured your primary residence against certain taxes and legal claims. If your heirs cannot find this proof, they might face heavy financial burdens that you worked hard to avoid.

The danger of lost documentation is real. Imagine an emergency where your family needs to prove the home's status, but the paperwork is buried in a box or lost in a computer crash. Without clear evidence of your homestead exemption filings, your family could lose thousands of dollars in tax savings. They might even risk the home's legal protection. A secure vault ensures your tax records and deeds are accessible exactly when they are needed most.

Organizing Your Property Records

You need one central place for your property's "keys to life." Use a simple checklist to ensure your vault is complete. You should upload your recorded deeds, title insurance policies, and approved homestead exemption applications. It's also smart to keep property tax receipts from the last 7 years. These records prove your history of residency and tax compliance.

Digital vaults do more than just store files. They use automated delivery features to notify your "Receivers" when a life event happens. This ensures your loved ones don't have to go on a scavenger hunt during a crisis. This level of organization is a core part of digital estate planning for modern families who want to avoid confusion and protect their heritage.

A Call to Action for Your Family’s Security

The homestead exemption is a powerful tool for your current budget and your future legacy. It keeps money in your pocket today and shields your home for the next generation. Don't let your hard work go to waste because of a missing document. Moving from uncertainty to total peace of mind is a simple step. You can start protecting your most important documents with IronClad Family today. Ensuring your family's story continues without interruption is the greatest gift you can leave behind.

Take Control of Your Home’s Future

Claiming your homestead exemption is a vital step in guarding your family's financial health. In many states, this simple filing can shield up to $500,000 of your home's value from creditors and lower your annual tax bill by hundreds of dollars. Most jurisdictions require you to submit your paperwork between January 1 and March 15 to qualify for the current year. Keeping your property records and proof of residency organized is the only way to avoid missing these critical deadlines.

Your home represents a lifetime of hard work and memories. We help you protect that legacy with zero-knowledge encryption that ensures total privacy for your records. Our tools cover estate planning requirements in all 50 states and feature automated emergency delivery so your loved ones are never left without answers. It's about moving from a place of uncertainty to a state of absolute preparedness. Your family's digital DNA deserves a permanent, secure home.

Learn how to protect your family’s most important documents

You've taken the first step by learning your rights. Now, you can rest easy knowing your home and your history are safe.

Frequently Asked Questions

Does a homestead exemption expire or do I have to renew it every year?

Most states don't require you to renew your homestead exemption every year once the county approves your initial application. In Florida, your exemption renews automatically as long as your residency status doesn't change. You only need to refile if you move to a new home or if the name on your property deed changes due to marriage or divorce.

Can I have a homestead exemption on two different properties if I live in both?

You cannot claim a homestead exemption on two different properties at the same time. These tax breaks are strictly for your primary residence where you spend the majority of your time. If you try to claim two, you could face heavy back taxes and legal penalties. Most states require you to live in the home for at least 183 days a year to qualify.

What happens to my homestead exemption if I move my home into a Living Trust?

Your homestead exemption usually stays in place when you move your home into a Living Trust, but the trust must be structured correctly. You must remain the beneficiary and keep the legal right to live in the home for the rest of your life. In states like California, the law allows the exemption to carry over to a revocable trust so your tax benefits remain secure.

Is the homestead exemption the same thing as a homestead declaration?

A homestead exemption is not the same thing as a homestead declaration. The exemption reduces your property taxes by lowering your home's taxable value in the eyes of the county. A declaration is a legal document you file to protect your home equity from certain creditors. For example, in Massachusetts, a filed declaration protects $500,000 in equity, while the automatic protection is only $125,000.

Can creditors take my home if I have a homestead exemption filed?

Creditors can still take your home in specific situations even if you have a homestead exemption filed. This protection doesn't apply to your mortgage lender, the IRS, or contractors who have a valid mechanic's lien on the property. It primarily stops general creditors, like credit card companies or medical bill collectors, from forcing a sale to pay off debts that aren't tied to the house.

How much money can I actually save on my property taxes with this exemption?

You can typically save between $200 and $1,500 per year on your property taxes depending on your local tax rates. In many Texas counties, a $40,000 exemption on a home's value leads to several hundred dollars in annual savings. These numbers change based on your school district and county rules, so check your local assessor's 2024 rate table for exact figures in your area.

What is the deadline to file for a homestead exemption in 2026?

The deadline to file for a homestead exemption in 2026 is March 1 in states like Florida and April 30 in states like Texas. You should aim to submit your paperwork by January 15 to avoid any processing delays or late fees. Missing these dates usually means you'll have to wait an entire calendar year to see the savings reflected on your property tax bill.

Do I lose my homestead exemption if I rent out a room in my house?

You won't lose your homestead exemption if you rent out a room, provided the home remains your main residence. Most tax authorities require you to live in the property for more than six months of the year to keep your status. If you move out and rent the entire house to a tenant, you'll lose the tax benefit and the creditor protection almost immediately.